How Do Cashback Apps Make Money? (And Is It Safe to Use?)

Getting real money back from an app sounds too good to be true. But once you understand how cashback apps actually work, the scepticism disappears.

This guide explains how cashback apps make money, why the system is safe, and who's paying for your rewards.

The Myth - Free Money vs. What's Really Happening

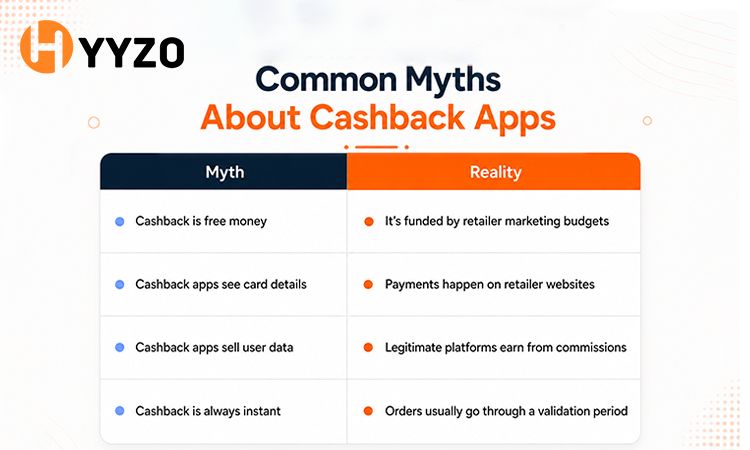

Nobody is losing money to give you cashback. Most first-time users assume cashback must come with a hidden catch because getting money back after shopping feels unusual. In reality, the cashback is simply a portion of the retailer's marketing budget being shared with the customer.

This is pure affiliate marketing at work. The money comes from a marketing budget that brands were already spending. Traditional ads cost money whether or not anyone buys. The cashback route is more reliable; brands only pay when a real sale happens. What you receive is your share of their advertising expense, redirected through a different channel.

How Do Cashback Apps Make Money? The Core Business Model

The cashback app business model works on a performance basis.

Brands like Flipkart, Myntra, and Croma have a high cost per acquisition (CPA) when running traditional ads. They pay to put ads in front of people, most of whom don't buy anything. With a cashback platform, the deal is different: the brand only pays a retail commission after a sale is confirmed.

The cashback website or platform earns that commission. It keeps a small cut for operations and passes the rexst back to the user. The entire cashback app business model is performance-based, with no cost to the shopper.

Revenue Streams: How Cashback Platforms Generate Profit

The platform earns from all four streams without touching your wallet. This is what makes the merchant partnership model sustainable. Multiple revenue sources mean the platform can continue passing the highest possible share of commissions back to shoppers.

The Technical Process: How Your Purchase Is Tracked

When you tap through a cashback app to a store, a unique, encrypted tracking link is generated. This sends a non-identifying token to the affiliate network, which notifies the retailer that the sale came from the platform. No personal profile is accessed. The system only exchanges transactional data - the sale amount and a session ID.

The Lifecycle of a Secure Cashback Transaction

- You open the cashback app and select a validated merchant partner

- An encrypted tracking token registers your exit click to the merchant store

- You complete your order through the store's standard checkout

- The merchant confirms the sale and passes the calculated commission back to the platform

This is exactly how cashback sites work at a technical level. A clean chain of anonymous confirmations, no personal data changes hands. How cashback sites work is designed to be invisible to the user - you shop, the token confirms, and money arrives.

Is Cashback Safe? Unpacking the Data Privacy Question

Yes. And here's why that answer holds up structurally.

Many shoppers worry that cashback apps need access to bank accounts, card details, or payment passwords. Legitimate cashback platforms don't process your payments at all. The purchase still happens directly on the retailer's website or app.

Legitimate platforms prioritise Hyyzo data protection and similar privacy standards because they make far more money from their Myntra affiliate and Flipkart commission relationships than they could ever earn from selling your personal data. Selling data to brokers would violate app store regulations, break financial data privacy laws, and destroy long-term partnerships with major retailers. There are far more benefits to maintaining a long-term brand partnership than to collecting user data.

Top platforms use data encryption to protect user profiles, and they never request or store card numbers or payment passwords. The only financial identifiers used during cashback are your UPI ID or bank routing details for the payout, and even those only flow in one direction, into your account.

The Economics of Safety - Real ₹ Math

Here's a concrete example using a ₹5,000 electronics purchase via a cashback platform:

Traditional Ad Route: The brand spends approximately ₹600 on unverified Facebook or Google clicks to acquire the same customer. No sale is guaranteed.

The Cashback Route:

The platform nets ₹150 on a clean, legal sale. Legit cashback apps in India that operate on this model earn consistently without needing to touch user data. Selling profiles for micro-rupees when ₹150 per transaction is available cleanly makes no business sense at all.

Common Myths About Cashback Apps

How Hyyzo Protects Your Shopping Data

Hyyzo's customer safety is built into the architecture from the ground up, enabling secure shopping via Hyyzo means the system is specifically designed to never expose your actual payment credentials at any stage of the checkout.

The app never views, stores, or requests raw card numbers or banking passwords. Payouts are processed via direct UPI aliases and IFSC-based bank integrations, both of which allow the system to push money into your account but not pull anything out. This bank-grade security model means your account details are never exposed to the app's internal system.

This surprises many new users, who assume cashback platforms process payments. In reality, the retailer's payment gateway handles the transaction, while the cashback platform only receives confirmation that a purchase took place.

The only data the platform actually touches is the transaction token from the affiliate network and your withdrawal address. Nothing else.

The Final Word on Cashback Legitimacy

Cashback apps are not a scam. They're a modern version of referral-based marketing, paid for entirely by brand marketing budgets. Hyyzo customer safety standards exist specifically to close the trust gap for new users.

Is cashback safe? Yes, if you use platforms that earn from brand commissions, not user data. Understand the model once, verify their privacy terms, and let corporate marketing budgets cover your savings.

Frequently Asked Questions

Q1. Why do stores pay cashback websites commissions?

The website's commissions come down to performance guarantees. Stores pay because it's a zero-risk model for them. They only hand over a commission after a verified purchase happens. Compared to traditional ad spend on digital platforms with no sale guarantee, cashback platforms deliver a confirmed customer and only then collect a fee. This is why legit cashback apps that Indian users trust continue to grow year on year.

Q2. Do cashback apps sell your personal data to third parties?

Reputable platforms don't. Their business depends on long-term affiliate relationships with major brands. Selling data would violate app store regulations, break privacy laws, and permanently destroy those partnerships.

Q3. How does Hyyzo make money if it gives cashback to users?

Hyyzo acts as a verified marketing partner for 200+ brands. When you complete a purchase, the brand pays a bulk referral fee to Hyyzo. Hyyzo keeps a small operational share and passes the remaining amount directly to your wallet. It's a standard split commission model.

Q4. Is it safe to link a bank account to cashback apps for withdrawals?

Yes. The app only needs your UPI ID or IFSC code to push cashback into your account. No permission to pull funds from your account is ever required.

Q5. Can cashback apps steal your credit card info during a purchase?

No. The app redirects you to the official merchant site through an encrypted tracking link. Your card details go straight into the retailer's checkout gateway. The cashback app only sees the transaction confirmation.

Q6. Are free cashback apps a scam or a trap?

No. The model is free because brands fund everything. The store gets a verified customer, the platform gets a referral fee, and you get paid from that fee. All three parties benefit from one transaction. It's a sustainable model, not a trap, as long as the platform earns revenue from brands rather than from user data.